VAT RATE UK – How Much VAT you Must Charge?

VAT must be charged on goods and services if your business is VAT registered in the UK. The rate you apply depends on the type of item or service offered.

Use the UK VAT Calculator to compute accurate amounts for standard, reduced, or zero-rated supplies.

Current VAT Rates in the UK

There are three main VAT rates in the UK: 20%, 5%, and 0%. These apply depending on the product category and service type.

- Standard rate 20%

- Reduce rate by 5%

- Zero rate 0%

Standard Rate

The standard VAT rate is 20% which is applied on most of the goods and services. When you purchase these goods and services 20% of the amount goes to VAT.

Change in VAT rate in the UK over the period

| YEAR | STANDARD VAT RATE |

| 1973 | 10% |

| 1974 | 12.5% |

| 1979 | 15% |

| 1991 | 17.5% |

| 2008 | 15% |

| 2010 | 17.5% |

| 2011 | 20% |

| 2012 | 12.5% |

| Present | 20% |

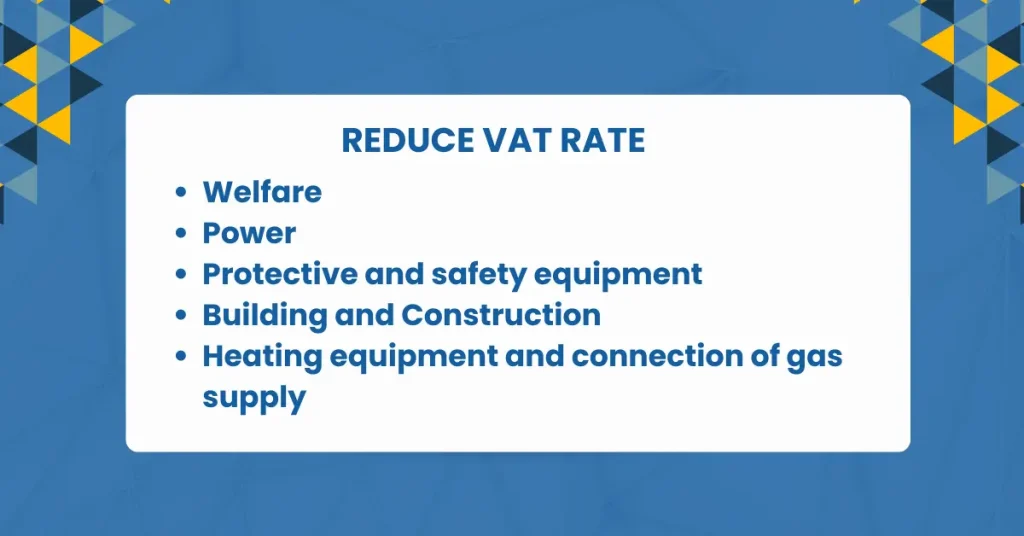

Reduced Rate – 5%

The 5% reduced VAT rate applies to specific items such as fuel, mobility aids, and building materials.

Categories include:

Welfare

- Mobility aids for elderly persons

- Smoking cessation aids like nicotine patches

Domestic Power

- Gas and electricity for residential use

- Heating oil and solid fuels

- Applicable in both the UK and Northern Ireland

Energy-Saving Materials

- Boiler systems, pipework, radiators

- Solar, wind, or hydro-based heating

Safety Equipment

- Carrycots with restraints

- Children’s car seats and booster seats

Building and Construction

- Renovations on empty dwellings

- Conversions increasing number of dwellings

- Gas reconnections

Reduced rates for energy-saving materials in Northern Ireland remain at 5%

Reference: VAT Notices 701/57, 708/6

For the people living in Northern Ireland reduced rate of energy-saving materials is 5%

Zero Rate – 0%

Zero-rated supplies carry 0% VAT, but businesses may still reclaim input VAT.

Categories include:

Charities

- Fundraising sales, advertising for charities

- Charity shop sales of donated items

Source:

VAT Notice 701/58, VAT Notice 708

Welfare

- Equipment for blind or disabled persons

- Building services for disabled people

Source:

Notice 701/7 VAT, VAT Notice 701/32

Health

- Dispensing prescriptions

- Sanitary products and incontinence pads

Source:

VAT Notice 701/31, VAT Notice 701/57, VAT Notice 701/7, VAT Notice 701/18,

Utilities

- Sewerage services

- Water for residential use

Source:

Energy-Saving Materials

Insulation, draught proofing

Solar panels, water turbines

Energy-saving materials installed in dwellings and buildings used for a relevant residential purpose

Building and Construction

- Sale or lease of new buildings for charities

- New homes and residential conversions

- Home adaptations for disabled people

Source:

VAT Notice 742, VAT Notice 708

Transport and Vehicles

- Passenger transport (10+ passengers)

- Ship repairs and airship maintenance

- Civil aircraft and caravans

Source:

VAT Notice 744C

Freight

- Freight transport to or from a place outside the UK

- Freight containers — sale, lease, or hire to a place outside the UK and the EU

- International freight transport that takes place in the UK and its territorial waters

Source:

VAT Notice 744B, VAT Notice 703/1, VAT Notice 744B

TRAVEL

- Passenger transport in a vehicle, boat or aircraft that carries not less than 10 passengers

Source:

VAT Notice 744A

Vehicles

- Aircraft repair and maintenance

- Airships — sale or charter

- Caravans (more than 7 meters long or more than 2.55 meters wide)

- Civil aero planes — sale or charter

- Helicopters — sale or charter

- Houseboats — sale or let out on hire

- Military airplanes — sale or charter

- Ship repairs and maintenance

- Shipbuilding — 15 tons or over gross tonnage

Source:

VAT Notice 744C

Printing and Publishing

- Brochures, newspapers, books

- Children’s picture books and sheet music

Source:

VAT Notice 701/10

Clothing and footwear

- Babywear

- Children’s clothes and footwear

Source:

VAT Notice 714

Protective and Safety Equipment

- Cycle helmets — CE marked

- Motorcycle helmets that meet safety standards

- Protective boots and helmets for industrial use

Source:

VAT Rates by Sector

| Sector | Typical Rate | Example Items |

|---|---|---|

| Retail | 20% | Electronics, clothing |

| Health | 0% | Prescriptions, maternity products |

| Construction | 0% / 5% | New builds, energy-saving installations |

| Charity | 0% | Fundraising goods, donations |

| Energy | 5% | Domestic fuel, energy-saving materials |

| Travel | 0% | Public passenger transport |

| Hospitality | 12.5% (2024) | Accommodation, food, drink |

| Printing & Books | 0% | Books, maps, newspapers |

| Children’s Goods | 0% | Car seats, clothes, safety gear |

Use the VAT Flat Rate Scheme if your turnover qualifies and you want simplified accounting.

Conclusion

VAT rates in the UK affect pricing, billing, and VAT reclaim for registered businesses. Understanding the correct rate 20%, 5%, or 0% ensures compliance and effective financial planning.

The standard rate applies to most goods and services. The reduced rate benefits utilities, welfare, and safety products. The zero rate supports basic needs, health, and education.

Refer to How to Register for VAT for setup guidance or use the UK VAT Calculator to run exact figures for billing.

FAQs

The current standard VAT rate is 20%.

The reduced rate is 5%, used for utilities, welfare, and energy-saving items.

Zero-rated items include books, babywear, basic food, and public transport.

It started at 10% in 1973 and has changed several times, now set at 20%.

Between December 2008 and December 2009, as part of a financial stimulus.

From July 2020 to September 2021 for hospitality and leisure sectors.

12.5% applies to food, accommodation, and drink services.

Yes. Schemes like the VAT Flat Rate Scheme help simplify VAT for eligible businesses.

Same VAT rates apply online and in-store standard, reduced, or zero.

Yes. Pricing reflects VAT rules and must be adjusted by businesses accordingly.